Sunday, October 28, 2007

Tuesday, October 16, 2007

Saturday, September 29, 2007

Cash Reserve Ratio(crr)hike/cut?

What is CRR?

Indian banks are required to hold a certain proportion of their deposits as cash. In reality they don’t hold these as cash with themselves, but with Reserve Bank of India (RBI), which is as good as holding cash. This ratio (what part of the total deposits is to be held as cash) is stipulated by the RBI and is known as the CRR, the cash reserve ratio. When a bank’s deposits increase by Rs100, and if the cash reserve ratio is 10, banks will hold Rs10 with the RBI and lend Rs 90. The higher this ratio, the lower is the amount that banks can lend out. This makes the CRR an instrument in the hands of a central bank through which it can control the amount by which banks lend.

Now take part in the following poll.

Indian banks are required to hold a certain proportion of their deposits as cash. In reality they don’t hold these as cash with themselves, but with Reserve Bank of India (RBI), which is as good as holding cash. This ratio (what part of the total deposits is to be held as cash) is stipulated by the RBI and is known as the CRR, the cash reserve ratio. When a bank’s deposits increase by Rs100, and if the cash reserve ratio is 10, banks will hold Rs10 with the RBI and lend Rs 90. The higher this ratio, the lower is the amount that banks can lend out. This makes the CRR an instrument in the hands of a central bank through which it can control the amount by which banks lend.

Now take part in the following poll.

Thursday, September 27, 2007

Saturday, September 22, 2007

>Rakesh Jhunjhunwala

It is 12.30 pm at RaRe Enterprises, Nariman Bhavan. There are five monitors showing more red than blue. The market is facing a blood bath. The Sensex is falling. In the thick of the action, Rakesh Jhunjhunwala turns from these screens, he is unruffled.

There is a massacre happening as investors lose wealth but Mr Jhunjhunwala looks at you almost bored and says "lets not discuss the markets". The biggest investor in India is chewing paan as he loses wealth on his screens. He lights a cigarette. He loosens his white shirt. He has not worn a tie for the last five years.

"I know I am losing wealth but should I let this bother me? I don't think so. I would be crazy to look at my wealth like this. I believe that India stands on strong fundamental grounds and over a period things are only positive. But please do not interpret this as Rakesh Jhunjunwalla is saying that the Sensex is going to touch 40000. Some day it may touch. But who knows when?"

For a man who purchased Tata Tea for Rs 5000 when he was only fifteen years old, Rakesh Jhunjhunwala has a total networth of ap-proximately Rs 6000 crore along with his wife Rekha Jhunjhunwala. The exact value of the portfolio is something he doesn't like to talk about.

He doesn't have any rules for his science of investing. But his ap-proach is fundamental and takes a long-term view thus he is also re-ferred as the Warren Buffet of India. Jhunjhunwala has never met Warren Buffet but admires and even follows his style of investment.

"Don't insult the great man by comparing me to him. I am young and I'm constantly learning. There is so much to learn from others." He pauses and refuses a phone call from a big corporate house in India. "But at the end of the day I want to be only Rakesh Jhunjhunwala and nobody else", he says.

Retail investors, analysts and fund managers always want to know what he is buying. Everybody wants to be a part of Rakesh's stocks. He knows that. He leans back and looks at you and tells you that he is not an advisor or a fund manager.

He and his wife came into the limelight with Crisil Limited. At the end of April 2005 he was holding 14.26% of the company, accounting for Rs 70 crore. In the same year the couple made Rs 27 crore after they sold out to the S&P open offer at Rs 775 per share. Today his in-vestment in Crisil is worth more than 200 crore and the holding accounts for 7.63% of the entire company. In all the companies that he has invested, it is this investment that has given him his famed mo-ments.

In India, bull runs have been associated with certain individuals. In the nineties it was Harshad Mehta and in early 2000 it was Ketan Parekh. But Jhunjhunwala does not like to be associated with any booms. He believes that the market is above individuals. Individuals can be associated to excesses in the markets, but not to the phase of the markets itself, he believes. It is like if the market is at a P/E multiple of 20, an individual might just make investors believe that the P/E should be 22. He thinks that individuals who believe that they are bigger than the markets do not last for a long time.

"The market is rational. An individual can never be smarter than the market", he says and his phone rings. Someone wants to sell him a credit card or personal loans. He politely refuses and drags on his cigarette.

"The market is about greed and fear. Sometimes there is too much greed and sometimes there is too much fear. It has a lot to do with the psychology of the market. You have to sometimes read the market like you read an individual", he adds.

But Mr Jhunjhunwala has not taken any courses in psychology or behaviorial finance to understand the psychology of the market. He has always believed that psychology cannot be learnt in classrooms. He has learnt his lessons in finance by practicing them and never believed in borrowed wisdom. He has liked his experience first hand. "I have experienced the markets from its core. You know I was there during the day of the bomb blasts when it happened. I have seen ups and downs so my understanding of the market is from being in there".

That is probably why international fund managers like to spend time with him to understand the Indian equity market. He meets at-least two international fund managers a week. Probably that is where he markets or tries to sell the India story to the global equity fund managers. He doesn't like it when he is referred in this context.

"How can you sell the Indian equity to the global fund manager? Is it an FMCG product like toothpaste or a shampoo? These fund managers are here because they believe in the fundamentals of the country. Not because a Rakesh Jhunjhunwala wants them to buy Indian equity". He gets slightly excited.

Incidentally, foreign investors are selling Indian equity as global markets are facing a liquidity crisis. Those who have purchased the India story are jittery. Highly leveraged funds that invest into global markets based on borrowed money are facing the heat. They have purchased assets that they are not able to value. They don't even un-derstand the nature of these assets.

As the ground beneath their feet starts to shake, Rakesh Jhunjhunwala sits firm. He was in Lonavala watching movies when the crisis was very severe. He is patient and knows that this shall also pass. The red on the screen will turn to blue. The market will once again be the winner. Mr Jhunjhunwala will remember this. His greatest fear - he might fall prey to his own philosophy. The market will remain above all individuals.

At a time when the market is going through volatility and an uncertain phase, Jhunjhunwala has no advice for the investors. "I don't advice anybody. I don't manage anybody's money. I manage my wife's money because I don't have a choice." He smiles and stubs his cigarette

There is a massacre happening as investors lose wealth but Mr Jhunjhunwala looks at you almost bored and says "lets not discuss the markets". The biggest investor in India is chewing paan as he loses wealth on his screens. He lights a cigarette. He loosens his white shirt. He has not worn a tie for the last five years.

"I know I am losing wealth but should I let this bother me? I don't think so. I would be crazy to look at my wealth like this. I believe that India stands on strong fundamental grounds and over a period things are only positive. But please do not interpret this as Rakesh Jhunjunwalla is saying that the Sensex is going to touch 40000. Some day it may touch. But who knows when?"

For a man who purchased Tata Tea for Rs 5000 when he was only fifteen years old, Rakesh Jhunjhunwala has a total networth of ap-proximately Rs 6000 crore along with his wife Rekha Jhunjhunwala. The exact value of the portfolio is something he doesn't like to talk about.

He doesn't have any rules for his science of investing. But his ap-proach is fundamental and takes a long-term view thus he is also re-ferred as the Warren Buffet of India. Jhunjhunwala has never met Warren Buffet but admires and even follows his style of investment.

"Don't insult the great man by comparing me to him. I am young and I'm constantly learning. There is so much to learn from others." He pauses and refuses a phone call from a big corporate house in India. "But at the end of the day I want to be only Rakesh Jhunjhunwala and nobody else", he says.

Retail investors, analysts and fund managers always want to know what he is buying. Everybody wants to be a part of Rakesh's stocks. He knows that. He leans back and looks at you and tells you that he is not an advisor or a fund manager.

He and his wife came into the limelight with Crisil Limited. At the end of April 2005 he was holding 14.26% of the company, accounting for Rs 70 crore. In the same year the couple made Rs 27 crore after they sold out to the S&P open offer at Rs 775 per share. Today his in-vestment in Crisil is worth more than 200 crore and the holding accounts for 7.63% of the entire company. In all the companies that he has invested, it is this investment that has given him his famed mo-ments.

In India, bull runs have been associated with certain individuals. In the nineties it was Harshad Mehta and in early 2000 it was Ketan Parekh. But Jhunjhunwala does not like to be associated with any booms. He believes that the market is above individuals. Individuals can be associated to excesses in the markets, but not to the phase of the markets itself, he believes. It is like if the market is at a P/E multiple of 20, an individual might just make investors believe that the P/E should be 22. He thinks that individuals who believe that they are bigger than the markets do not last for a long time.

"The market is rational. An individual can never be smarter than the market", he says and his phone rings. Someone wants to sell him a credit card or personal loans. He politely refuses and drags on his cigarette.

"The market is about greed and fear. Sometimes there is too much greed and sometimes there is too much fear. It has a lot to do with the psychology of the market. You have to sometimes read the market like you read an individual", he adds.

But Mr Jhunjhunwala has not taken any courses in psychology or behaviorial finance to understand the psychology of the market. He has always believed that psychology cannot be learnt in classrooms. He has learnt his lessons in finance by practicing them and never believed in borrowed wisdom. He has liked his experience first hand. "I have experienced the markets from its core. You know I was there during the day of the bomb blasts when it happened. I have seen ups and downs so my understanding of the market is from being in there".

That is probably why international fund managers like to spend time with him to understand the Indian equity market. He meets at-least two international fund managers a week. Probably that is where he markets or tries to sell the India story to the global equity fund managers. He doesn't like it when he is referred in this context.

"How can you sell the Indian equity to the global fund manager? Is it an FMCG product like toothpaste or a shampoo? These fund managers are here because they believe in the fundamentals of the country. Not because a Rakesh Jhunjhunwala wants them to buy Indian equity". He gets slightly excited.

Incidentally, foreign investors are selling Indian equity as global markets are facing a liquidity crisis. Those who have purchased the India story are jittery. Highly leveraged funds that invest into global markets based on borrowed money are facing the heat. They have purchased assets that they are not able to value. They don't even un-derstand the nature of these assets.

As the ground beneath their feet starts to shake, Rakesh Jhunjhunwala sits firm. He was in Lonavala watching movies when the crisis was very severe. He is patient and knows that this shall also pass. The red on the screen will turn to blue. The market will once again be the winner. Mr Jhunjhunwala will remember this. His greatest fear - he might fall prey to his own philosophy. The market will remain above all individuals.

At a time when the market is going through volatility and an uncertain phase, Jhunjhunwala has no advice for the investors. "I don't advice anybody. I don't manage anybody's money. I manage my wife's money because I don't have a choice." He smiles and stubs his cigarette

Monday, September 10, 2007

Sunday, August 19, 2007

Monday, August 13, 2007

Sunday, July 22, 2007

Wednesday, July 11, 2007

Sunday, July 08, 2007

Saturday, July 07, 2007

Monday, July 02, 2007

Sunday, July 01, 2007

Monday, June 25, 2007

Thursday, June 21, 2007

Monday, June 11, 2007

Sunday, June 03, 2007

Friday, June 01, 2007

Tuesday, May 29, 2007

Sunday, May 20, 2007

Tuesday, May 15, 2007

Saturday, May 12, 2007

Monday, May 07, 2007

Friday, May 04, 2007

AUROPHARMA

Weekly chart shows a Triangle possibility in AUROPHARMA target after breakout could be near to 1000.

Cheers

HUMBLY BOB

Thursday, May 03, 2007

Tuesday, May 01, 2007

ADOR WELDING

To read more about the Ador Welding fundamentals and research

http://aiiireports.blogspot.com/2007/05/spaador-welding.html

Wednesday, April 11, 2007

Saturday, April 07, 2007

Tuesday, April 03, 2007

Monday, March 26, 2007

RENUKA SUGAR ( Submerged in ELLIOT wave)

Hi friends,

Lets try to analyze the above script(RENUKA SUGAR)using Elliot wave.

The green arrows represent impulsive 1 and 3 wave.

The red arrows represent 2 and 4 corrective waves.

The dotted green arrows represent probable price movement in 5th wave.

There should not be a problem in figuring about the waves as its crystal clear from the chart above,

Lets have a closer view, we see that 4th wave is a triangle which broke up near 380.

This was given a buy here.(EETC Free Call)

Now with the help of FIB levels we can try to predict the subsequent movement of the price in 5th wave(triangle breakup initiated 5th impulsive wave)

Also see how important FIB level coincides with previous resistance point.

So here we saw how Elliot wave along with FIB can end up in a great trade.

FEW GOOD ELLIOT READS:

Bond Markets: Inverted Yield Curve Still Dangerous

http://www.elliottwave.com/a.asp?url=features/default.aspx?cat=pmp&dy=nth&cn=6bot

Does Elliott Wave Work Stock by Stock?

http://www.elliottwave.com/a.asp?url=features/default.aspx?cat=emw&dy=nth&cn=6bot

Relevant news on sugar sector

http://aiiireports.blogspot.com/2007/03/govt-to-create-buffer-stock-of-sugar.html

Regards

Rish

(EagleEyeTrade)

Wednesday, March 21, 2007

>JET AIRWAYS

To read about what a leading research house says about JET AIRWAYS

follow this link

http://aiiireports.blogspot.com/2007/03/clsa-report-on-jet-airways.html

CHEERS

Rish

Friday, March 16, 2007

Tuesday, March 13, 2007

Sunday, March 11, 2007

Friday, March 09, 2007

Sunday, March 04, 2007

Friday, March 02, 2007

Friday, February 23, 2007

JMFINANCIAL

JMFINANCIAL HAS GICEN BREAKOUT ONE CAN LONG THIS STOCK AT CMP OR ON SOME DIP SL 960 FOR A FIRST TARGET OF 1080.

ATLANTA

ATLANTA one down leg still pending traders can short this script after some rise with sl near 1150 for first target of 1000.

Thursday, February 22, 2007

Tata Motors pips Hyundai in Jan sales

Marking a first, Tata Motors has crept past Hyundai Motor India Ltd in domestic car sales in January to gain the coveted second slot in the Indian car market.

According to the Society of Indian Automobile Manufacturers, Tata Motors, whose range included the Indica hatchback, the Indigo sedan and the Marina station wagon, sold 17,673 units in January, which was marginally above Hyundai's total sales of 17,452 units.

The Tatas sold over 14,466 Indica cars, which was slightly lower than the sales of 14,592 units of the Santro hatchback in January.

However, Tata Motors gained in sales of midsized Indigo and Marina, clocking 3,207 units in January, against Hyundai's mid-sized car sales of 2,860 (this includes the Accent, Verna, Elantra and Sonata).

Analysts say the growing preference for diesel cars and better performance of Tata cars in particular has helped the company, whereas Hyundai has been unable to launch new models and suffered some production issues.

"Hyundai is upgrading capacity and will be able to ramp up production for domestic sales by the last quarter this year," said Huzaifa Suratwala of Emkay Share and Stock Brokers.

Wednesday, February 21, 2007

Citigroup Raises $1.29 Billion to Buy Real Estate in China, India, Asia

Citigroup Inc.'s property unit said it raised $1.29 billion for its first fund to invest in real estate and related assets in the Asia-Pacific region, with a focus on China and India.

Citigroup, the largest U.S. bank, and its investment professionals committed $200 million to the fund, CPI Capital Partners Asia Pacific LP, according to a statement from the New York-based bank. The fund will be managed by a Hong Kong-based team of more than 25 employees led by managing director David Schaefer. About 40 percent of the fund has been invested or pledged already.

Fund managers are trying to profit from fast-growing economies in Asia and capture more fee income from managing assets on behalf of pension funds seeking the annual returns of 10 percent or more that funds such as Citigroup's are designed to provide. Since the beginning of 2006, U.S. managers have raised more than $5 billion to invest in Asian real estate, according to Private Equity Intelligence Ltd. in London.

``Asia is a compelling market for private equity real estate investments,'' said Joseph Azrack, 59, president and chief executive officer of Citigroup Property Investors, in a statement.

Property Investment

Azrack, who came to Citigroup in 2004 from Boston-based AEW Capital Management LP, is expanding real estate offerings as Wall Street banks and buyout firms raise record funds for global property investment. Morgan Stanley is raising $8 billion for what would be the largest real estate fund of its kind and Goldman Sachs Group Inc. also is forming a new real estate fund. Blackstone Group LP, which bought Equity Office Properties Trust earlier this month in the largest-ever leveraged buyout, plans to raise about $10 billion for a new real estate fund this year.

Azrack's division oversees more than $9.8 billion and invests in publicly traded and closely held securities in a variety of asset types, including office, industrial, apartments, retail and hotels.

Citigroup also announced yesterday that it plans to raise $3.5 billion for a fund to invest in companies in emerging markets such as India, China, Estonia and Chile.

Citigroup will commit $1 billion to the fund, called Citigroup Venture Capital International Growth Partnership II LP, and expects to raise the rest from employees and clients, according to a marketing brochure.

In December, Citigroup Property Investors said it raised $2.1 billion for its first high-return real estate funds, one for Europe and the other for North America.

Citigroup Property Investors is part of Citigroup Alternative Investments, one of the bank's four main business divisions. Besides Hong Kong and New York, the property unit has offices in Shanghai, London and Los Angeles and a presence in Mumbai.

source:- bloomberg

Saturday, February 10, 2007

ONGC, Russian gas major sign pact

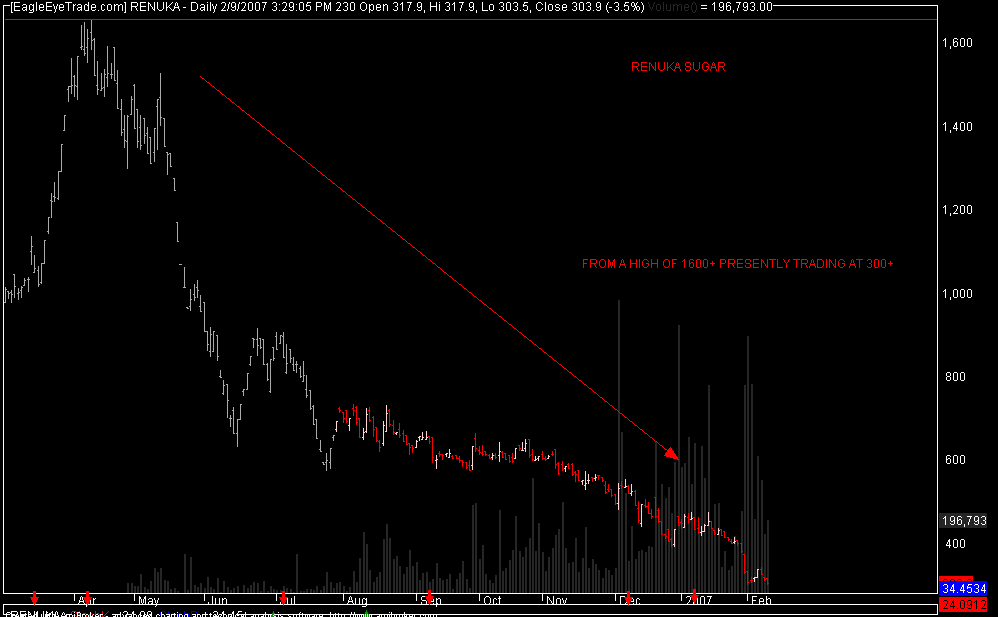

haunted sugar

In a phase where India stock market witnessed its fastest and biggest gain(Mad Bull),Sugar sector witnessed massive slump. Sugar has become one haunted sector where investors are scared even to look at.

In a phase where India stock market witnessed its fastest and biggest gain(Mad Bull),Sugar sector witnessed massive slump. Sugar has become one haunted sector where investors are scared even to look at.let me remind this sector used to be flavour of market , Traders & Investors used to swear on sugar sector performance.

I myself know many investors who are invested in sugar and yes at high rates and t

hey kept averaging it which eventually compounded the trouble as there was no revival in sugar sector stock prices(example averageing can be suicidal at times)all the sugar stocks are trading below there 52 week low and still they are not showing any resistance to fall.

hey kept averaging it which eventually compounded the trouble as there was no revival in sugar sector stock prices(example averageing can be suicidal at times)all the sugar stocks are trading below there 52 week low and still they are not showing any resistance to fall.READ MORE ABOUT SUGAR FALL Sugar may witness corrective phase.

In short sugar sector in BEAR GRIP (a phase in market where stock prices fall a

nd keep falling slowly which frustrates investors).It will be a long long way to recovery if at all things turn in sugar industry favour as every rise will attract selling from the ones struck in it for long time they will try to be the first to get relieved from the agony of holding a loss making stock for a long time, and this process continues till sellers get exhausted after that only we can witness fresh virgin upmove in sugar.

nd keep falling slowly which frustrates investors).It will be a long long way to recovery if at all things turn in sugar industry favour as every rise will attract selling from the ones struck in it for long time they will try to be the first to get relieved from the agony of holding a loss making stock for a long time, and this process continues till sellers get exhausted after that only we can witness fresh virgin upmove in sugar.check out the charts to see the deep ridges in sugar stock prices.

NOTE:-I myself was stuck in sugar but was brave enough to book loss in it :-) and yes quite relieved now after watching the outcome.

Thursday, February 08, 2007

JET AIRWAYS

jet airways consolidating in a triangle can breakup anytime buy with a sl below 780 for targets of 825, 850,900 respectively

cheers

rish

{kind=link}

Tuesday, January 30, 2007

FINANCIAL TECH

FINANCIAL TECH consolidating after a recent move buy near 1760-70 sl below 1740 first target near 1860

cheers

rish

There's no stopping the Indian IT juggernaut

IT software and services sector firms continue to be on a roll. Just when the market was expecting the December 2006 quarterly results to be a tame affair - primarily due to an appreciating rupee, rising attrition and wages and fewer billing days - IT majo rs, mid- and small-caps beat market expectations in many cases to post more-than-satisfactory results.

rs, mid- and small-caps beat market expectations in many cases to post more-than-satisfactory results.

IT bellwether Infosys Technologies set the ball rolling, weathering a rupee appreciation of 3.8 per cent to register a net profit of Rs 983 crore (Rs 9.83) - a sequential growth of 5.8 per cent in net profit and a 5.9 per cent sequential increase in its top line.

The sequential growth prompted the company to once again revise its guidance for the full year. It now expects to cross the $3 billion level (it has provided guidance of Rs 13,910-13,919 crore) for 2006-07.

Given the projected growth rate, its net profit alone will be around Rs 3,700 crore (Rs 37 billion) in FY07 (in FY03, its consolidated revenue was Rs 3,640 crore). A feather in its cap, Infosys was added to the Nasdaq-100 Index on December 18.

alone will be around Rs 3,700 crore (Rs 37 billion) in FY07 (in FY03, its consolidated revenue was Rs 3,640 crore). A feather in its cap, Infosys was added to the Nasdaq-100 Index on December 18.

The largest Indian IT firm Tata Consultancy Services, on the other hand, beat market expectations to become the first Indian IT company to clock $1 billion in revenues in a single quarter as it posted a net profit of Rs 1,105 crore (Rs 11.05 billion) for the quarter.

The IT behemoth thus crossed the $3 billion revenue mark in the first three quarters, registering an 8 .4 per cent sequential increase in its total revenues and 11.4 per cent q-o-q increase in net profit for Q3 FY07.

.4 per cent sequential increase in its total revenues and 11.4 per cent q-o-q increase in net profit for Q3 FY07.

TCS executives attributed the company's performance to a good business mix and continued better pricing. The company is on its way to become a $4 billion entity this financial year.

Wipro's global IT business, which includes IT and BPO services, grew 6.2 per cent q-o-q in Q3 FY07 with a net profit increase of nearly 7 per cent. HCL Technologies too reported a sequential top line growth of 6.2 per cent growth and a net profit growth of 18.7 per cent.

Satyam, on the other hand, was more disappointing with revenues rising 3.7 per cent q-o-q and a 5.45 per cent net profit growth. The rupee appreciation impacted all software companies, but that is not a matter of concern. Software companies are on a strong wicket and should keep clocking improvements going forward.

Success ingredients

Most of the recommendations of analysts, so far, remain in the "hold" or "buy" category.

What's working for all IT services firms (small or big) is their global delivery models and global delivery centres which helps them de-risk their businesses by expanding geographically, acquiring companies in their domain areas (be it major companies like Wipro or mid-caps like 3i Infotech, Subex Azure, i-flex, Four Soft or Tech Mahindra), winning larger deals (for instance, HCL Technologies, Tech Mahindra, TCS and Infosys have all struck multi-million dollar deals this quarter) and negotiating new contracts at billing rates that have increased 3-5 per cent and more.

For TCS, there was a 90 basis points expansion in EBITDA (earnings before tax, interest and depreciation) margins to 28.3 per cent in the third quarter. Over the last six months, the IT major has been able to expand margins by over 400 basis points.

According to ICICI Securities, the reasons include higher pricing, productivity improvements and an offshore shift (41.6 per cent of revenues in Q3 FY07, as against 41 per cent last quarter).

On the volume front, the management has ten deals ranging in size from $50-100 million. It is looking at strong growth in the Chinese and Latin American markets.

The number of clients contributing revenues of over $1 million in the case of Infosys has increased from 206 a year ago to 256, while the number of clients contributing revenues over $5 million has risen from 78 to 108 over the past 12 months. The company has 11 clients contributing over $50 million, against seven clients a year ago.

It also has two clients contributing greater than $100 million. Its billing rate for the quarter continued its upward trend with onsite rates increasing by 1.9 per cent q-o-q and offshore rates up by 1.7 per cent.

Infosys' billing rates have now seen upward movement for four consecutive quarters, which is particularly impressive, says Edelweiss Securities.

Satyam too has seen an offshore shift and lower employee costs powered margins despite the weakness in top line growth. It reported a strong 205 basis point expansion last quarter.

Employee costs reduced to 58.2 per cent of revenues from 61.3 per cent in Q2, as the impact of the Restricted Stock Units was largely factored in. The contribution of offshore business improved by 130o basis points, which helped in better margins, according to Angel Broking.Moreover, the Indian economy is booming. No doubt, there is pressure from the Democrats in the US on outsourcing, but it is not likely to make much of a dent on the top lines or bottom lines of Indian IT services companies, infer experts.

Further, the IT software exports business is well on course to achieve the ambitious target of $60 billion by 2010 is an oft-repeated statement by Nasscom.

The latest figures add more credence to this figure. The Indian domestic IT market is expected to exceed $15.9 billion in 2006-07 recording a 21 per cent growth.

Software and services (IT-BPO) exports are expected to exceed $31 billion in fiscal 2006-07 - a 32.6 per cent growth over last year's figure of $23.6 billion. So, to reach $60 billion in 2009-10, the Indian tech sector has to grow at slightly less than 25 per cent a year, which does not seem difficult.

Innovation holds the key

On the human resources front, TCS saw an attrition rate of 10.8 per cent, which is the lowest among IT firms. Other IT firms have seen attrition rates anywhere between 13-20 per cent. This remains a matter of concern.

On the flip side, though, the dearth of IT engineers is forcing the Indian and technology companies to recruit around 40,000-50,000 non-IT professionals and science graduates in this financial year, which is the highest by any industry in the country.

This is notwithstanding the fact the over 10 lakh (1 million) IT professionals are being churned out annually by IT and management institutes.

IT majors like Infosys, TCS, Tech Mahindra and Wipro are some companies recruiting non-IT personnel for IT jobs, while other IT companies and the unorganised sector is also close behind.

Healthy competition

Global consulting firm neoIT predicts that companies based in the West will take a keen interest in onsite set-ups to stay competitive as well as explore eastern markets, which are not only cost-effective delivery locations, but also rapidly emerging markets by themselves.

India will continue to lead the supplier market and Europe will continue to show a strong growth. Internationally, neoIT's report predicts that 2007 will see Russia emerge as a strong contender in the IT outsourcing market with an expected growth of 40-45 per cent in 2007.

It is currently the third largest IT outsourcing supply market, behind India and China. Russian IT companies specialise in high-end software and embedded software product development, which acts as a differentiator from lower-priced offerings from Indian companies, it says.

On the India front, the billing rates amongst the tier-1 India IT services providers too will go up by 3-4 per cent both for existing as well as new contracts in 2007, according to neoIT.

The study has attributed the growth in the billing rates to a growing demand for skilled resources, rise in wages, and increased overheads incurred in maintaining quality.

However, despite the hike, the offshore services providers will remain competitive against the global players, says Sabyasachi Satpathy, senior director, neoIT.

The positive sign is that India will remain the fastest-growing country in the Asia-Pacific region in terms of domestic IT spending and is expected to grow at 21.5 per cent to touch Rs 75,891 crore (Rs 758.91 billion), according to IDC.

In 2007, IDC predicts System Integration partners will aim to minimise costs by breaking down activities into smaller modules. Vendors like IBM have already come to market with such offerings. TCS, Wipro and HP are expected to follow suit in 2007 and this trend is expected to gain further momentum through the year.

It's a no-brainer that the operating profit and revenue margins of IT firms will decrease as they get increasingly bigger. However, what's heartening is that with every quarter, they have found better ways of dealing with margin pressure and have become more efficient.

Further, mid- and small-cap IT firms are unfurling their potential and should soon cover up for the excellent margins that the bigwigs will gradually give up with time.

A recent Forrester report concluded that global outsourcing will become the dominant form of IT delivery by 2012. The next quarter's figures would only add muscle to this prediction.

source :- business standard

rs, mid- and small-caps beat market expectations in many cases to post more-than-satisfactory results.

rs, mid- and small-caps beat market expectations in many cases to post more-than-satisfactory results.IT bellwether Infosys Technologies set the ball rolling, weathering a rupee appreciation of 3.8 per cent to register a net profit of Rs 983 crore (Rs 9.83) - a sequential growth of 5.8 per cent in net profit and a 5.9 per cent sequential increase in its top line.

The sequential growth prompted the company to once again revise its guidance for the full year. It now expects to cross the $3 billion level (it has provided guidance of Rs 13,910-13,919 crore) for 2006-07.

Given the projected growth rate, its net profit

alone will be around Rs 3,700 crore (Rs 37 billion) in FY07 (in FY03, its consolidated revenue was Rs 3,640 crore). A feather in its cap, Infosys was added to the Nasdaq-100 Index on December 18.

alone will be around Rs 3,700 crore (Rs 37 billion) in FY07 (in FY03, its consolidated revenue was Rs 3,640 crore). A feather in its cap, Infosys was added to the Nasdaq-100 Index on December 18.The largest Indian IT firm Tata Consultancy Services, on the other hand, beat market expectations to become the first Indian IT company to clock $1 billion in revenues in a single quarter as it posted a net profit of Rs 1,105 crore (Rs 11.05 billion) for the quarter.

The IT behemoth thus crossed the $3 billion revenue mark in the first three quarters, registering an 8

.4 per cent sequential increase in its total revenues and 11.4 per cent q-o-q increase in net profit for Q3 FY07.

.4 per cent sequential increase in its total revenues and 11.4 per cent q-o-q increase in net profit for Q3 FY07.TCS executives attributed the company's performance to a good business mix and continued better pricing. The company is on its way to become a $4 billion entity this financial year.

Wipro's global IT business, which includes IT and BPO services, grew 6.2 per cent q-o-q in Q3 FY07 with a net profit increase of nearly 7 per cent. HCL Technologies too reported a sequential top line growth of 6.2 per cent growth and a net profit growth of 18.7 per cent.

Satyam, on the other hand, was more disappointing with revenues rising 3.7 per cent q-o-q and a 5.45 per cent net profit growth. The rupee appreciation impacted all software companies, but that is not a matter of concern. Software companies are on a strong wicket and should keep clocking improvements going forward.

Success ingredients

Most of the recommendations of analysts, so far, remain in the "hold" or "buy" category.

What's working for all IT services firms (small or big) is their global delivery models and global delivery centres which helps them de-risk their businesses by expanding geographically, acquiring companies in their domain areas (be it major companies like Wipro or mid-caps like 3i Infotech, Subex Azure, i-flex, Four Soft or Tech Mahindra), winning larger deals (for instance, HCL Technologies, Tech Mahindra, TCS and Infosys have all struck multi-million dollar deals this quarter) and negotiating new contracts at billing rates that have increased 3-5 per cent and more.

For TCS, there was a 90 basis points expansion in EBITDA (earnings before tax, interest and depreciation) margins to 28.3 per cent in the third quarter. Over the last six months, the IT major has been able to expand margins by over 400 basis points.

According to ICICI Securities, the reasons include higher pricing, productivity improvements and an offshore shift (41.6 per cent of revenues in Q3 FY07, as against 41 per cent last quarter).

On the volume front, the management has ten deals ranging in size from $50-100 million. It is looking at strong growth in the Chinese and Latin American markets.

The number of clients contributing revenues of over $1 million in the case of Infosys has increased from 206 a year ago to 256, while the number of clients contributing revenues over $5 million has risen from 78 to 108 over the past 12 months. The company has 11 clients contributing over $50 million, against seven clients a year ago.

It also has two clients contributing greater than $100 million. Its billing rate for the quarter continued its upward trend with onsite rates increasing by 1.9 per cent q-o-q and offshore rates up by 1.7 per cent.

Infosys' billing rates have now seen upward movement for four consecutive quarters, which is particularly impressive, says Edelweiss Securities.

Satyam too has seen an offshore shift and lower employee costs powered margins despite the weakness in top line growth. It reported a strong 205 basis point expansion last quarter.

Employee costs reduced to 58.2 per cent of revenues from 61.3 per cent in Q2, as the impact of the Restricted Stock Units was largely factored in. The contribution of offshore business improved by 130o basis points, which helped in better margins, according to Angel Broking.Moreover, the Indian economy is booming. No doubt, there is pressure from the Democrats in the US on outsourcing, but it is not likely to make much of a dent on the top lines or bottom lines of Indian IT services companies, infer experts.

Further, the IT software exports business is well on course to achieve the ambitious target of $60 billion by 2010 is an oft-repeated statement by Nasscom.

The latest figures add more credence to this figure. The Indian domestic IT market is expected to exceed $15.9 billion in 2006-07 recording a 21 per cent growth.

Software and services (IT-BPO) exports are expected to exceed $31 billion in fiscal 2006-07 - a 32.6 per cent growth over last year's figure of $23.6 billion. So, to reach $60 billion in 2009-10, the Indian tech sector has to grow at slightly less than 25 per cent a year, which does not seem difficult.

Innovation holds the key

On the human resources front, TCS saw an attrition rate of 10.8 per cent, which is the lowest among IT firms. Other IT firms have seen attrition rates anywhere between 13-20 per cent. This remains a matter of concern.

On the flip side, though, the dearth of IT engineers is forcing the Indian and technology companies to recruit around 40,000-50,000 non-IT professionals and science graduates in this financial year, which is the highest by any industry in the country.

This is notwithstanding the fact the over 10 lakh (1 million) IT professionals are being churned out annually by IT and management institutes.

IT majors like Infosys, TCS, Tech Mahindra and Wipro are some companies recruiting non-IT personnel for IT jobs, while other IT companies and the unorganised sector is also close behind.

Healthy competition

Global consulting firm neoIT predicts that companies based in the West will take a keen interest in onsite set-ups to stay competitive as well as explore eastern markets, which are not only cost-effective delivery locations, but also rapidly emerging markets by themselves.

India will continue to lead the supplier market and Europe will continue to show a strong growth. Internationally, neoIT's report predicts that 2007 will see Russia emerge as a strong contender in the IT outsourcing market with an expected growth of 40-45 per cent in 2007.

It is currently the third largest IT outsourcing supply market, behind India and China. Russian IT companies specialise in high-end software and embedded software product development, which acts as a differentiator from lower-priced offerings from Indian companies, it says.

On the India front, the billing rates amongst the tier-1 India IT services providers too will go up by 3-4 per cent both for existing as well as new contracts in 2007, according to neoIT.

The study has attributed the growth in the billing rates to a growing demand for skilled resources, rise in wages, and increased overheads incurred in maintaining quality.

However, despite the hike, the offshore services providers will remain competitive against the global players, says Sabyasachi Satpathy, senior director, neoIT.

The positive sign is that India will remain the fastest-growing country in the Asia-Pacific region in terms of domestic IT spending and is expected to grow at 21.5 per cent to touch Rs 75,891 crore (Rs 758.91 billion), according to IDC.

In 2007, IDC predicts System Integration partners will aim to minimise costs by breaking down activities into smaller modules. Vendors like IBM have already come to market with such offerings. TCS, Wipro and HP are expected to follow suit in 2007 and this trend is expected to gain further momentum through the year.

It's a no-brainer that the operating profit and revenue margins of IT firms will decrease as they get increasingly bigger. However, what's heartening is that with every quarter, they have found better ways of dealing with margin pressure and have become more efficient.

Further, mid- and small-cap IT firms are unfurling their potential and should soon cover up for the excellent margins that the bigwigs will gradually give up with time.

A recent Forrester report concluded that global outsourcing will become the dominant form of IT delivery by 2012. The next quarter's figures would only add muscle to this prediction.

source :- business standard

Subscribe to:

Posts (Atom)